Understanding the Now-Concluded UK Help to Buy Scheme: Pros and Cons

The Help to Buy initiative enabled first-time home ownership dreams until new applications to it closed on 31 October 2022. By helping with deposits through equity loans, it improved purchasing power for constrained first-time buyers. Now, as attention shifts to comparable schemes, it is worthwhile reviewing Help to Buy's structure, benefits accessed, limitations faced and legacy impact.

The Help to Buy initiative enabled first-time home ownership dreams until new applications to it closed on 31 October 2022. By helping with deposits through equity loans, it improved purchasing power for constrained first-time buyers. Now, as attention shifts to comparable schemes, it is worthwhile reviewing Help to Buy's structure, benefits accessed, limitations faced and legacy impact.

Help to Buy Equity Loan Scheme Mechanics

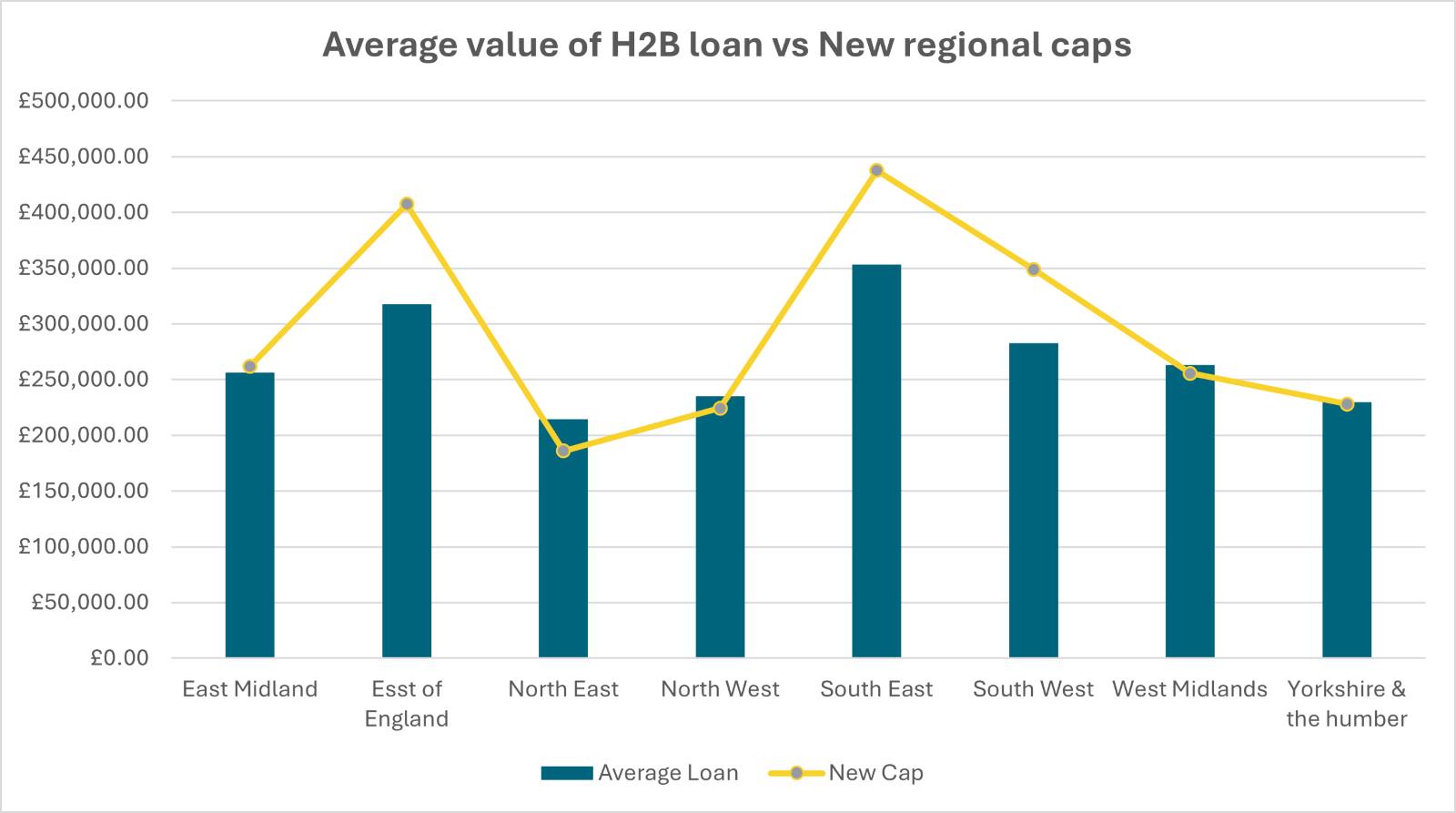

The scheme saw the UK government offer eligible first-time buyers an equity loan of up to 20% of a new-build home's value (40% of value in London) against a second charge on the property. Qualifying new build homes from registered housebuilders in England were subject to maximum price caps, ranging from £186,000 in the North East to £349,000 in the South West to £600,000 in London¹.

The scheme enabled purchases with just a 5% deposit. For the remaining deposit, - up to 15% of value outside London and 35% in London, - the government equity loan provided under Help to Buy was interest-free for the first five years. After this initial period, an annual interest rate of 1.75% was applied to the outstanding equity loan amount in the sixth year. From the seventh year onwards, the interest rates were the previous year’s interest rate increased by the annual rate of inflation (based on the Consumer Price Index) plus 2%. Thus, for year 7, if the inflation rate was 2.5%, the year 6 interest rate of 1.75% would be increased by 4.5% (inflation rate of 2.5% + 2% = 4.5%), resulting in a year 7 interest rate of 1.83% (1.75 x 1.045 = 1.83%).

The equity loan was also subject to the first-time home buyer taking out a traditional first charge repayment mortgage of up to 75% of the purchase price (with a minimum of 25%).

The equity loan amount that was repayable was based on the market value of the home at the time of repayment. Thus, for example, if the original equity loan was 15% of the purchase price and it was repaid in full 10 years later (upon the sale of the property), the equity loan repayment amount would be 15% of sale price. If the home price increased, the repayment amount increased and vice versa.

Source² : Knight frank

Why the Scheme Ended

After being extended repeatedly since 2013, Help to Buy applications closed permanently in October 2022, with March 2023 as the deadline for associated property purchase completions. As objectives of the program lifting over 350,000 families across the homeownership threshold have been achieved, the government is now diverting funding towards other first-time buyer incentives.

Pros Accessed by Homebuyers

With lower deposit requirements, owning a home became more affordable. Additionally, interest rate waivers helped to lower the initial housing costs, making it easier for buyers to get started. Moreover, new-build quality homes offered an added appeal with modern and upgraded features.

Cons and Criticisms Faced

Surging house prices led to an escalation of outstanding equity loan balances owed. Once the interest-free period elapsed, borrowers struggled with the interest payments. Additionally, options for the borrowers were limited due to restrictions imposed on participating developer projects. Furthermore, borrowers faced several obstacles during later remortgaging due to the attached second charges.

First-Time Homeownership Schemes Now Available

With the Help to Buy Scheme closed to new applicants, UK homebuyers may wonder what government incentives are still available to support their homeownership dreams. Various initiatives exist aimed at easing first property purchases.

Shared Ownership

Shared Ownership is a scheme that allows people to purchase an initial share in a home of between 25-75%, based on the deposit and mortgage payments they can afford. The developer owns the remaining share of the property, and the buyer pays rent on this share to the developer as the landlord. As the buyer's financial situation improves, they can increase their share by buying more of the developer's share, a process known as 'staircasing'. Correspondingly, as the developer's share decreases, the rent decreases. This scheme is a practical alternative to traditional home purchasing methods and is available across the UK. It can be an ideal solution for those who cannot afford a property outright, as it requires a smaller mortgage and deposit for the purchase of the initial share.

Forces Help to Buy

Serving military personnel can avail of interest free loans of up to 50% of their annual salary, up to a maximum of £25,000, to apply to deposits and property purchase costs such as solicitors’ and estate agents’ fees.

Lifetime ISAs

A long-term Individual Savings Account for under 40s enables savings of up to £4,000 annually, with a 25% bonus from the government added to that amount. This accumulates tax-free towards a first home purchase costing up to £450,000 with a mortgage.

Self-Build and Custom Housebuilding Loans

In England, Scotland, and Wales, aspiring homeowners looking to build their homes can benefit from equity loans for between 5% and 40% of estimated land and building costs not exceeding £600,000 (where the building costs cannot exceed £400,000). This empowers individuals to create tailored living spaces and encourages innovative housing solutions.

First Homes Scheme

Under this scheme, a first-time buyer may be able to buy their first home at a 30% - 50% discount to its market value. They would need to be able to qualify for a mortgage covering at least 50% of the house price and not earn more than £80,000 per year before tax (£90,000 in London). Local councils might set other local eligibility criteria, such as prioritising key workers, local residents and those on lower incomes.

In summary, with the end of equity loan approach of Help to Buy, evolving mechanisms carry its vision forward of smoothing the difficult path towards turning renters into first-time homeowners in an expensive UK property landscape.

FAQs:

Q: Who qualified for the Help to Buy Scheme?

A: Initially, the Scheme was open to both first-time buyers and existing homeowners. Over time, eligibility was refined to focus on first-time buyers only, with purchase price caps introduced to ensure the Scheme benefited genuine entry-level buyers.

Q: Why did the government conclude the Help to Buy Scheme?

A: The Scheme was concluded after successfully helping a significant number of families onto the homeownership ladder. The government decided to channel funds into other housing support programs for first-time buyers.

Q: Are there any exemptions from the stamp duty under the Scheme?

A: First-time buyers benefited from stamp duty relief under certain conditions, which varied over time with changes in government policy.

References:

1. The homebuyers' guide to the Help to Buy: Equity Loan 2021 to 2023 | Homes England | Updated 16 March 2023

Ready to see what Pauzible could unlock?

Explore how releasing equity from your home could support your plans, with flexible, transparent options designed around you.

No obligation. Just a clear view of what might be possible.