Understanding Mortgage Closing Documents

A mortgage closing, also known as completion, is the final step in the process of buying a home with a mortgage. This is when the legal transfer of the property from the seller to the buyer is finalised. The process involves several steps.

The Closing Explained

A mortgage closing, also known as completion, is the final step in the process of buying a home with a mortgage. This is when the legal transfer of the property from the seller to the buyer is finalised. The process involves several steps. First, all the financial transactions are settled and the buyer's solicitor will ensure that all parties have signed all the necessary documents. These include the mortgage deed and transfer deed. These documents are important as they legally bind the buyer to the mortgage terms and transfer the property's ownership. Any outstanding fees will be paid, including any solicitor's fees and stamp duty land tax. Once everything is signed and all funds have been transferred, the seller can hand over the keys to the property. The buyer's solicitor will then register the transfer deed with the Land Registry which completes the transaction.

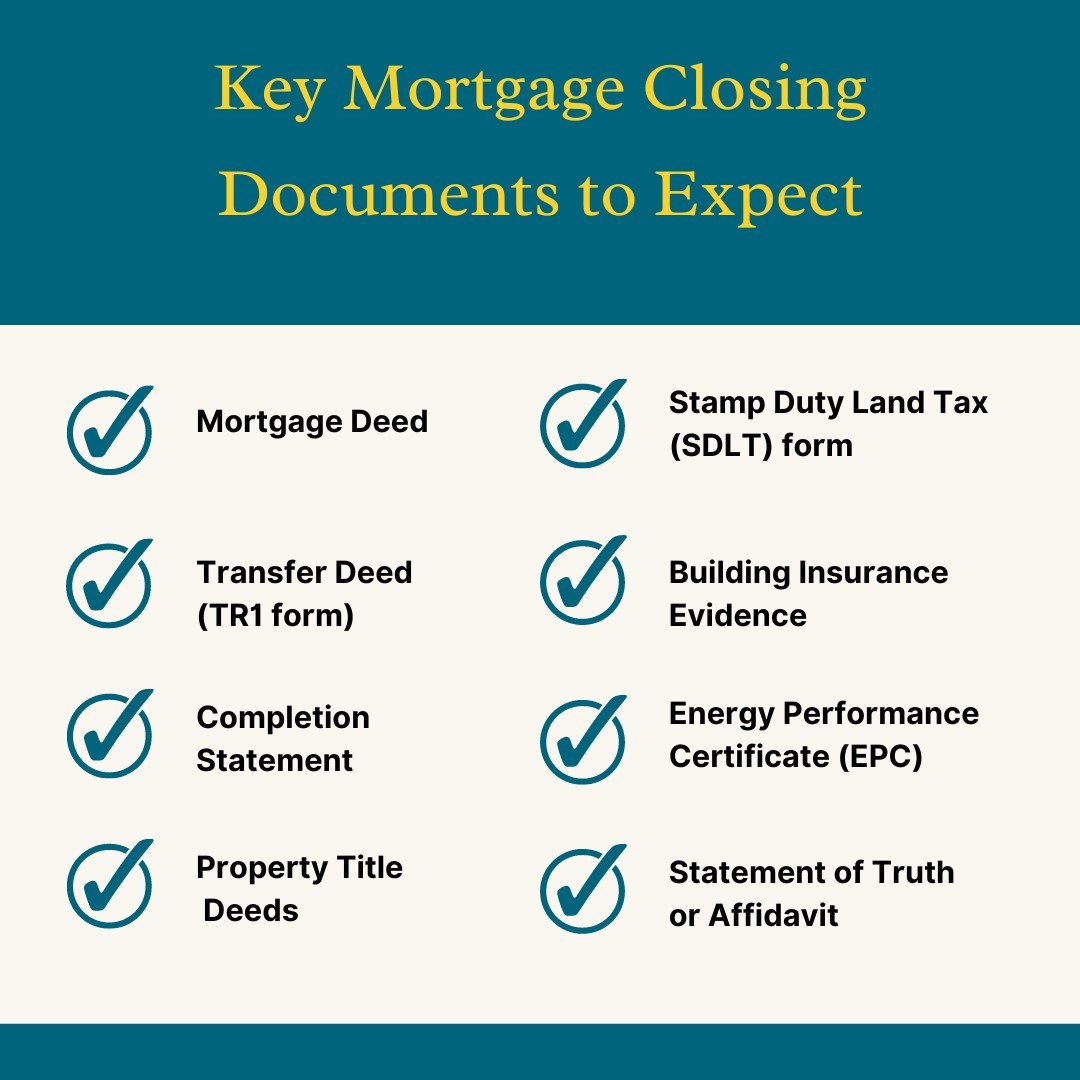

Key Documents to Expect

Key documents to expect during the mortgage closing process include:

- Mortgage Deed: The mortgage deed is the document that secures the loan by linking it to the property being purchased, essentially making it collateral for the loan. The mortgage deed specifies important details of the money being lent to the home buyer. It will specify the loan amount, interest rate and repayment terms. The mortgage deed contains the conditions and legal obligations for maintaining the property and repayment obligations. It describes in detail the rights of both the lender and the borrower if repayment is not made. The mortgage deed will also include a legal description describing the property.

- Transfer Deed (TR1 form): This document transfers property ownership from the seller to the buyer. Both parties must sign it for the transfer to be legal. The document will clearly identify all signing parties, describe the property, describe the conditions under which the transfer is being made and provide any specific declarations by either party.

- Completion Statement: A completion statement is a detailed financial summary that outlines all the monetary transactions involved in purchasing a property. This statement is important as it itemizes how the total amount due at completion is calculated. It includes the purchase price of the property, adjustments for items such as prepaid taxes or utilities by the seller, solicitor's fees, stamp duty land tax, and any other costs associated with the transaction, such as search fees or Land Registry fees. For the buyer, it shows the deposit already paid, the mortgage amount provided by the lender, and the balance that must be paid at completion. For the seller, it lists the remaining mortgage balance, agent's fees, and other deductions, showing the final amount they will get from the sale. The completion statement is important because it ensures all parties to the transaction understand the financial details before the property transfer is finalised.

- Property Title Deeds: The title deeds include a record of the owners of the property. This helps ensure that the seller has the legal right to transfer the property. The title provides details of the property description, including boundaries, the size of the property, the type of building, and any additional structures or land included in the parcel. The title will also contain important information regarding easements, covenants and restrictions. Easements are rights that come with the property to give access to others, such as utility companies. These types of easements give utility companies the right to access a certain part of the property to maintain utility lines. Covenants or restrictions dictate what the owner can or cannot do with the property, such as restrictions on building extensions or alterations. The title deed will also list any charges and liens associated with the property. It will disclose any mortgages or liens against the property which need to be cleared during the purchase process to ensure a clean title. Lastly, the title will include any leasehold information. This will include lease terms, lease length, any ground rent payable and lease agreement conditions.

- Searches and Survey Reports: Searches and survey reports provide information about the property to potential buyers. Searches are legal inquiries made by the buyer's solicitor to various authorities. These searches reveal important details about the property, including local planning decisions and potential developments in the area. They also uncover environmental concerns like flooding risks and any financial liabilities attached to the property, such as unpaid local taxes. On the other hand, survey reports are detailed examinations of the property's physical condition. They assess the structural integrity of the building, identify any defects or necessary repairs, and provide an evaluation of the property's market value. Together, searches and survey reports help buyers understand the property's legal standings and physical condition. This helps guide the decision-making process and helps them avoid potential problems after purchase.

- Stamp Duty Land Tax (SDLT) form: The Stamp Duty Land Tax form is used to declare the amount of stamp duty owed to the government following a property transaction. Stamp duty is a tax paid on properties over a certain price. The SDLT form must be filled out and submitted to HM Revenue and Customs (HMRC) by the buyer or their solicitor. This form calculates the tax based on the property's purchase price and must be submitted and the tax paid within 14 days after the completion of the purchase. Properly filling out and submitting this form is important to ensure all legal tax obligations are met during the property buying process.

- Building Insurance Evidence: This evidence is usually a certificate or a policy from the insurance provider detailing the coverage amounts, what is included and excluded, and the period for which the insurance is valid. Insurance is important as it protects the structure of the home against damage from events like fire, flood and other risks. Lenders typically require evidence of insurance before finalising a mortgage to protect their investment.

- Energy Performance Certificate (EPC): The seller supplies an energy performance certificate that provides information on a home's energy usage and carbon dioxide emissions. This document will also contain recommendations and suggestions for reducing energy use. Properties are ranked from A to G, with A being the most energy-efficient.

Reviewing Your Documents

It is important to review all closing documents with your solicitor. This ensures that you fully understand the terms and conditions of your mortgage and the legal obligations and rights pertaining to the property. Your solicitor may find potential problems with the property’s title or boundaries. Reviewing documents in advance provides an opportunity to resolve errors or negotiate terms before the final commitment.

Beyond Completion

After the completion and the signing of all relevant documents, there are a few additional steps. The solicitor will register the transfer of ownership with the Land Registry, ensuring that government records reflect the change in property ownership. Additionally, your solicitor will handle the payment of Stamp Duty Land Tax, if applicable. You should receive a copy of all signed documents for your records, and it is always best to store these securely. The mortgage lender will set up your account and initiate the agreed upon repayment schedule.

Conclusion

Reviewing and understanding closing documents is crucial to ensuring a smooth transaction. Each step requires careful attention and understanding. Being informed and prepared can take the stress out of purchasing a home, especially if this is your first time.

FAQs:

Q. What are mortgage closing documents?

A: Mortgage closing documents are legal papers for finalising a property purchase with a mortgage. These documents are essential for transferring ownership from the seller to the buyer. Key documents typically include the mortgage deed, which outlines the mortgage terms; transfer deed, which transfers property ownership; completion statement, which details the financial transactions; and title deeds, which include ownership of the property and conditions related to it.

Q. What happens after mortgage closing?

A: After mortgage closing, the buyer’s solicitor will register the change of ownership with the Land Registry, which officially documents you as the property's new owner. Additionally, your solicitor will pay Stamp Duty Land Tax on your behalf if applicable. You will also receive copies of all signed documents for your records. Keeping these documents safe is important as they are proof of your ownership and contain important information about the mortgage agreement. Finally, the mortgage lender will set up your mortgage account and mortgage payments will begin.

Ready to see what Pauzible could unlock?

Explore how releasing equity from your home could support your plans, with flexible, transparent options designed around you.

No obligation. Just a clear view of what might be possible.