An Introduction to How Shared Ownership Mortgages Work

Shared ownership mortgages combine the affordability of renting with the flexibility of increasing your ownership stake in the property gradually, over time.

Buying a home is a common aspiration. However, the high cost of property relative to earnings makes it very difficult for some to save enough money for a deposit and get a large enough mortgage to be able to buy a property outright. This is where the shared ownership scheme comes in. It is designed to help people buy a home by allowing them to purchase relatively small shares of the property initially and over time instead of the whole of it at once.

How does a Shared Ownership Mortgage Work?

A shared ownership mortgage is a special type of mortgage that helps you buy a part of a home that falls under the shared ownership scheme. It helps people get on the property ladder without the need for a large deposit and large mortgage initially.

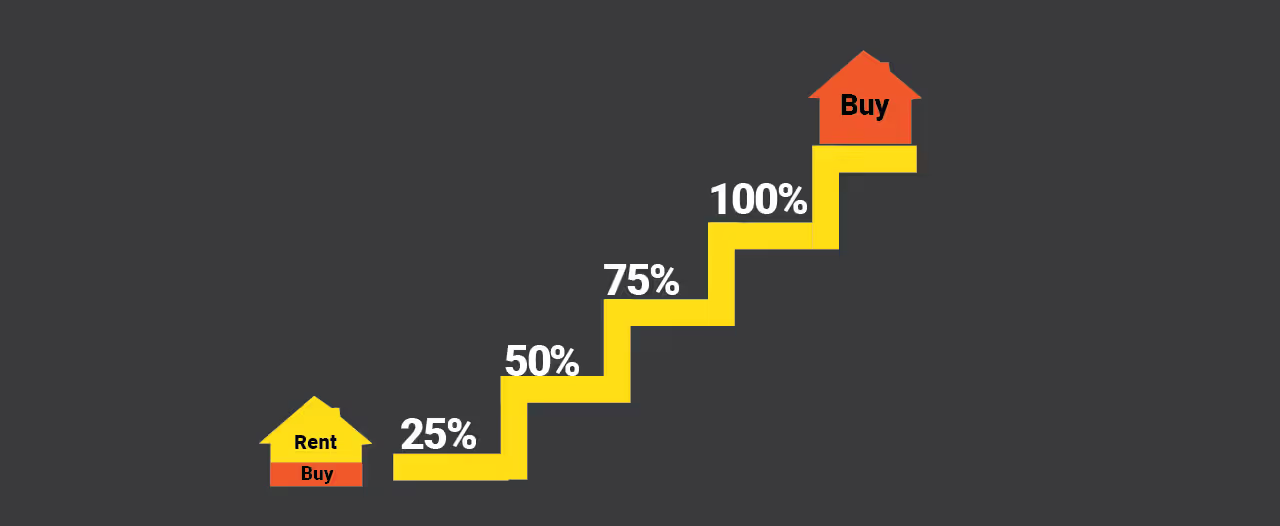

Under the shared ownership scheme, you can buy a part of the home, usually between 25% and 75% initially, although sometimes as low as 10%, and pay rent on the remaining share, which is owned by a housing association. Because you are only buying a part of the home initially, the initial deposit and mortgage you need is relatively small. A shared ownership mortgage usually requires a deposit of only 5% to 10% of the share of the home you are buying. At the same time, the rent on the share of the property that you are not buying could be lower than the average market rate, thus making the route to home ownership potentially more affordable.

As time goes on, you can buy more shares in the property, when you can afford it. This is called "staircasing”. Each time you buy an additional share of the home, you might also be able to increase your existing mortgage or possibly remortgage. In any event, the purchase of an additional share will decrease the rent you pay because you own more of the property. If you eventually buy 100% of the property, you will no longer have any rent to pay.

Who Is Eligible for Shared Ownership?

Shared ownership is designed to help people who are struggling to buy a home outright. Certain eligibility criteria must be met to qualify for shared ownership, including those set out below.

Your household income must be below a certain level. If you live outside London, your household income must be £80,000 a year or less. If you live in London, the income limit is £90,000 a year. This income limit includes the earnings of everyone in the household, so it is important to consider this when applying to buy a home under the shared ownership scheme.

In addition, you need to be a first-time buyer or someone who used to own a home but cannot afford to buy a home now to meet their needs. If you currently own a home, you must sell it before applying to buy a home under the shared ownership scheme to suit your housing needs.

Of course, you must be able to afford the costs of buying a share in the property, including the deposit, mortgage payments and rent. Lenders will consider your income, savings and expenses to assess if you can afford the costs associated with shared ownership. They will also look at your credit history.

It is also worth noting that some properties are only available to specific groups of people. For example, some shared ownership homes might be reserved for key workers such as nurses, teachers or police officers. Others might be available only to people who live or work in the local area.

If you meet the criteria, shared ownership could be a good option for you. However, it is important to consider all the costs and responsibilities involved before making a decision.

How Much Deposit Do I Need for Shared Ownership?

When you buy a home through shared ownership, the deposit you need is smaller than if you were buying the entire property outright. This is because the deposit is based on the share of the property you are buying, not its full value. For example, if a home is worth £200,000 and you are buying a 50% share, you are purchasing a share worth £100,000. In addition, deposit percentage requirements are usually relatively low. Thus, in this example, if the lender were to ask for a 5% deposit, you would need to have saved only £5,000 (5% of £100,000). If you bought a 25% share of the same property, your deposit would be even lower, around £2,500. This smaller deposit requirement makes means that shared ownership is more accessible to people who might struggle to save for a larger deposit. It is important to remember that some lenders might require a larger deposit, while others might be more flexible. It is always a good idea to shop around and compare different mortgage deals to find one that works for you.

Benefits of Shared Ownership

Shared ownership has several benefits that make it an attractive option for people who want to buy a home but cannot afford to do so outright.

One of the most significant benefits is the lower deposit. Because you are only buying a share of the property and the deposit percentage requirements are usually low, the deposit you need is much smaller than if you were buying the whole home. This makes it easier to save up and get started on the property ladder for first-time buyers, for example.

Another benefit is the lower monthly payments. Since your mortgage is based on the share you are buying, your mortgage payments are correspondingly lower. Furthermore, the rent you pay on the part of the property you do not own but rent can be below the market rate. These factors could make your home ownership costs more affordable.

Shared ownership also offers flexibility. You can start by buying a small share in the property and then buy more shares, over time, as your financial situation improves. Eventually, you might be able to buy the whole property, at which point you will no longer have any rent to pay.

Another advantage is that, unlike renting, where you do not own any part of the property, shared ownership means you own a share of the home. This gives you more security and a stake in the property’s value.

Considerations

The rent on the portion owned by the housing association can go up annually in line with inflation, potentially making it hard during periods of high inflation. If you want to buy more of the property later, you will need to pay for legal fees and property valuations each time. You might have to pay service charges for things like maintaining shared areas or services, adding to your costs. You will need to get permission from the housing association to make significant changes to the property and you will typically not be able to rent out your property. Such factors can make shared ownership less straightforward than it seems, so it is important to weigh them carefully before choosing this option.

How can I find a shared ownership mortgage?

- Housing Associations: Many housing associations offer shared ownership properties and can guide you through the process of finding a mortgage. They can sometimes have partnerships with certain lenders who provide shared ownership mortgages.

- Mortgage Brokers: A mortgage broker can help you find a shared ownership mortgage that suits your needs. They have access to a wide range of lenders and can compare different deals to find the best one for you.

- High Street Banks and Building Societies: Many major banks and building societies offer shared ownership mortgages. You can visit their websites or branches to explore your options and see what products they have available.

- Online Mortgage Comparison Websites: Websites such as Money Super Market, Compare the Market and Money.co.uk allow you to compare shared ownership mortgage deals from different lenders in one place. This can help you find a competitive offer.

- Local Authority Websites: Some local councils provide information on shared ownership schemes and may direct you to lenders who offer shared ownership mortgages.

Conclusion

Shared ownership is a valuable option for many people looking to buy a home. For some, it offers a way to get on to the property ladder with a smaller deposit and lower monthly payments than would otherwise be the case, making homeownership more accessible. Through the staircasing process, you can increase your ownership of the property gradually and eventually own it outright. Nevertheless, it is important to consider carefully whether shared ownership is the right choice for you. Make sure you understand the costs, responsibilities and benefits, and any potential constraints and drawbacks before making a final decision.

Sources:

https://www.gov.uk/shared-ownership-scheme

https://www.barclays.co.uk/mortgages/shared-ownership-mortgages/

Ready to see what Pauzible could unlock?

Explore how releasing equity from your home could support your plans, with flexible, transparent options designed around you.

No obligation. Just a clear view of what might be possible.