SVR Mortgages: Hidden Gem or Financial Trap?

Discover the pros and cons of Standard Variable Rate mortgages. Learn when to stay on SVR and when to switch for optimal financial planning.

A mortgage term is usually 25 years long, assuming the borrower will not be older than 70 when the term ends. A fixed or tracker mortgage rate “deal period”, on the other hand, is much shorter, usually only two or five years long. The mortgage rates that apply during a mortgage term, therefore, are usually a succession of two- or five-year deal period fixed or tracker rates. Tracker mortgage rates consist of the Bank of England base rate, which is subject to change, plus a fixed margin. The Standard Variable Rate (SVR), also known as the “reversion rate”, is the default interest rate that lenders apply to a mortgage when a fixed or tracker rate deal period ends, and the borrower has not selected a new fixed or tracker rate from a menu of deals offered by the lender for a follow-on deal period. SVRs are usually higher than deal period fixed or tracker rates.

How SVRs Work

The SVR can change at any time at the lender's discretion. While SVRs often reflect the Bank of England's base rate, they are not directly linked to it. This means lenders can adjust the SVR in response to factors such as their cost of borrowing. SVRs can also vary between lenders. Each lender has its own methodology for calculating its SVR, including taking into account its lending criteria, costs, profit margins and other factors.

The majority of borrowers usually choose a succession of short-term deal period fixed or tracker rates instead of choosing or defaulting to the SVR. The SVR can apply to any mortgage, whether for a property that is owner-occupied or used for buy-to-let purposes, if the borrower does not select a new short-term rate.

Advantages and Disadvantages

Advantages:

- Flexibility: Borrowers on SVRs can usually repay any amount of their mortgage early, including full redemption, without incurring an early repayment charge. This can be particularly beneficial for those planning to move or pay off their mortgage soon. This flexibility also applies to deal period tracker rates, although not fixed rates.

Disadvantages:

- Unpredictability: The unpredictability of rate changes can lead to higher monthly payments if the SVR increases. This lack of certainty can make budgeting and financial planning more challenging, especially for borrowers on tight budgets. This unpredictability also applies to deal period tracker rates, although SVRs tend to be higher than tracker rates.

When is Staying on an SVR a Good Option?

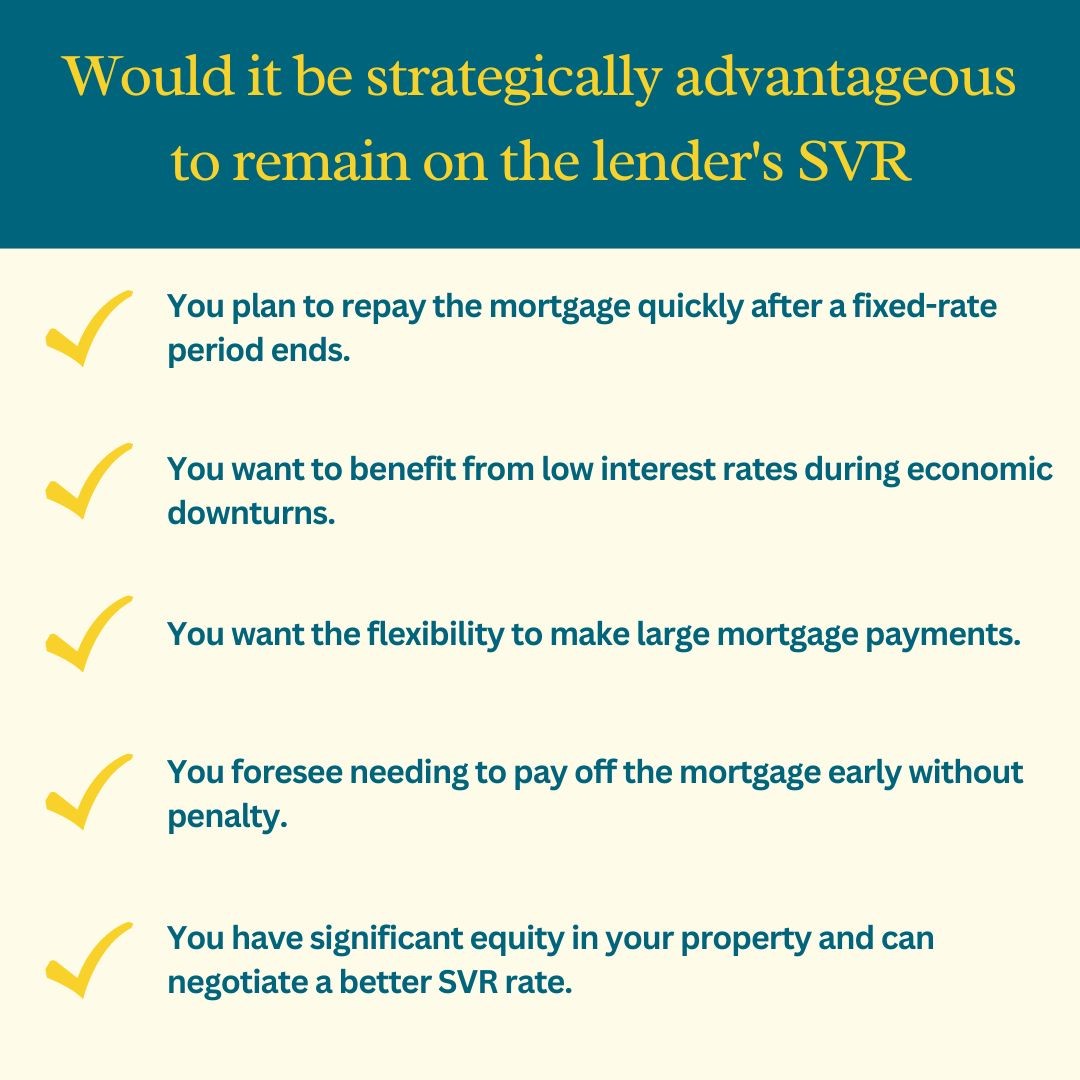

Choosing to be on an SVR (or a tracker rate) might be suitable if you plan to pay off your mortgage soon after the end of a short-term fixed rate deal period or take advantage of low rates during a period of declining rates. It also offers flexibility for those who want to make significant overpayments or foresee a change in circumstances requiring them to pay off their mortgage early without incurring penalties. If you have substantial equity in your property, you may be able to negotiate a more favourable SVR rate with your lender. Lenders are often more inclined to offer better rates to borrowers with lower loan-to-value (LTV) ratios, as they pose a lower risk.

When to Consider Switching from an SVR

It is typically wise to consider switching from an SVR (or tracker) if you are on a significantly higher interest rate compared to available fixed rate deals, especially when rates are forecasted to rise. Fixing your rate can protect you against future rate increases during the applicable deal period and make your monthly payments predictable, which can be particularly beneficial to borrowers on a tight budget.

Important Considerations

Before opting to stay on an SVR, it is crucial to consider your financial situation, risk tolerance and plans. Assess whether the flexibility of an SVR outweighs the potential for rising costs and if the SVR is competitive compared to other products, such as a tracker. Understanding the lender's policies regarding SVR rate changes and the factors that influence their decisions can also be helpful. There are several factors to be considered:

1. Financial Situation: Your current income stability and cash flow can significantly impact the suitability of an SVR mortgage. If your income is variable or subject to fluctuations, an SVR mortgage may offer the flexibility you need without incurring penalties for repayment changes. This is also an advantage provided by a tracker rate, but a fixed rate mortgage may provide more certainty and budgeting ease if your income is stable and predictable.

2. Risk Tolerance: Your comfort with uncertainty in interest rates plays a vital role. If you prefer stability and predictability in your financial planning, an SVR (or tracker) may not align with your risk profile, as rates can fluctuate based on lender discretion and market conditions. However, an SVR (or tracker) could be a viable option if you have a higher risk tolerance and are willing to accept potential rate changes in the belief that rates are set to decline.

3. Future Plans: If you anticipate significant changes in your circumstances, like a move, the flexibility of an SVR (or tracker) to make overpayments or settle without an early repayment charge can be beneficial. However, it is also important to assess the potential for rate increases that could impact your future financial commitments.

4. Interest Rate Forecast: Understanding market trends and forecasts for interest rates can help you gauge the potential cost of an SVR (or tracker) in the future. With the Bank of England's base rate at 5.25% as of the second quarter of 2024 and indications of variable rates such as SVR and tracker rates trending upwards, it is important to consider the likelihood of further rate increases and how that could affect your budget.

5. Equity Level: The more equity you have in your property, the lower your loan-to-value (LTV) ratio. This can affect your deal period fixed and tracker rates, but potentially also the SVR. Higher equity could give you more negotiating power to secure a lower SVR with your lender.

FAQs

Q. What is a Standard Variable Rate (SVR) Mortgage?

A. The Standard Variable Rate (SVR), also known as the “reversion rate”, is the default interest rate that lenders apply to a mortgage when a fixed rate or tracker rate deal period ends, but the borrower has not selected a new fixed or tracker rate from a menu of deals offered by the lender for a follow-on deal period. SVRs are usually higher than deal period fixed or tracker rates. The SVR can change at any time at a lender's discretion. While SVRs often reflect the Bank of England's base rate, they are not directly linked to it.

Q. What are the Advantages and Disadvantages of an SVR Mortgage?

A. As with tracker rates, advantages include flexibility. Borrowers can usually overpay or redeem the mortgage early without a penalty charge. Disadvantages involve uncertainty, as rates can increase at any time, leading to higher payments.

Q. Should I Stay on an SVR Mortgage?

A. It depends on your financial situation. Staying on an SVR (or tracker) may be sensible if you are planning to sell soon after the end of a fixed rate deal period or if variable interest rates are low and expected to decline. However, if SVR (or tracker) rates are high, it may be cost-effective to switch to a fixed rate deal.

Q. How can I track changes in the Bank of England base rate and how they might affect my SVR mortgage?

A. You can track base rate changes on the Bank of England's website and financial news outlets. While SVRs are not directly linked to the base rate, they are often influenced by changes to it.

Ready to see what Pauzible could unlock?

Explore how releasing equity from your home could support your plans, with flexible, transparent options designed around you.

No obligation. Just a clear view of what might be possible.